.jpg?ext=.jpg)

© ipopba/iStock/Getty Images Plus

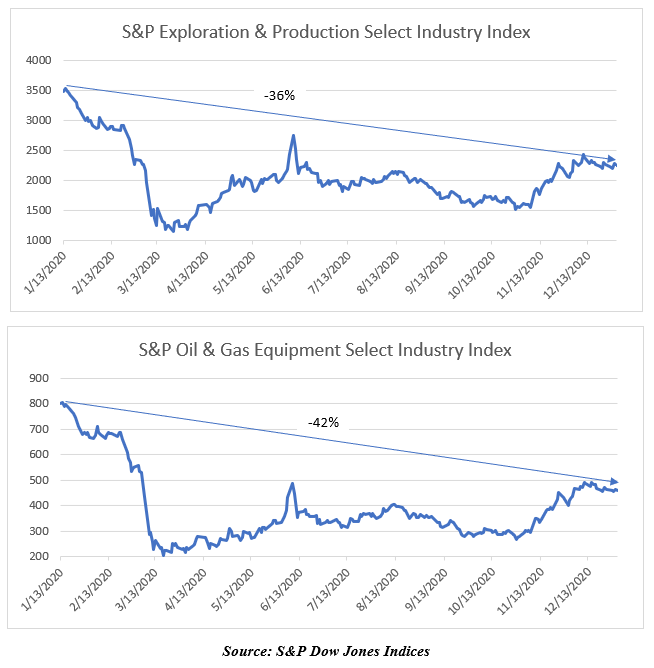

Market equity prices and indices continued to decrease for many energy companies during 2020. For instance, between January 13, 2020, and December 31, 2020, the S&P Oil & Gas Exploration and Production Select Industry Index decreased by approximately 36%, inclusive of a rebound in the second half of the year. Likewise, the S&P Oil & Gas Equipment Select Industry Index decreased by 42% during this same timeframe, also inclusive of a rebound in the second half.

With this continued decrease in market capitalizations, coupled with commodity price declines in recent years, auditors and regulators will continue to focus on impairment testing for goodwill and long-lived assets on the balance sheets of energy-focused companies.

Under Accounting Standards Codification Topic 350, Intangibles: Goodwill and Other (ASC 350), goodwill is tested for impairment at least annually or when a triggering event dictates. Under Accounting Standards Codification Topic 360, Property, Plant and Equipment (ASC 360), long-lived assets are tested for impairment when a triggering event dictates. Continued declines in market prices such as those that occurred during most of 2020, along with associated changes in industry fundamentals (e.g., changes in drilling plans for E&P companies and changes in customer buying patterns for oilfield services companies), may qualify as triggering events.

When navigating the goodwill impairment test under ASC 350, some common issues that companies may encounter include (but are not limited to) the following:

- Reconciliation of Fair Value to Market Capitalization: As part of their ASC 350 testing procedures, public companies will need to reconcile their estimated fair value conclusions with their market capitalization. This could mean that companies may even need to estimate the fair value of reporting units that don’t have goodwill to ensure the reasonableness of their overall valuation assumptions and financial projections.

- Weighted Average Cost of Capital: Estimating discount rates in the current economic environment can also pose a challenge, given recent changes in the risk-free rate, increased volatility (via the beta), and changes to guideline company debt-to-equity ratios. As such, additional scrutiny will likely be applied to discount rate calculations.

Likewise, companies that are performing a long-lived asset impairment test under ASC 360 should consider the following:

- Composition of Asset Groups: The testing level for ASC 360 purposes is referred to as an asset group, which could include both tangible and intangible assets. Company management should ensure that the composition of their asset groups is appropriate.

- Financial Projections: Auditors will continue to closely scrutinize the cash flow projections utilized by companies in their undiscounted cash flow test, also known as the recoverability test, for ASC 360 purposes. One key element of the cash flow projections is the length of time that the forecast entails. The life of the cash flow projections should mirror the expected economic life of the primary asset within the asset group. Therefore, care should be taken to ensure that the cash flow projections reflect an appropriate economic life.

Publicly and privately held companies need to adequately address their year-end 2020 goodwill and long-lived asset impairment testing procedures. Doing so in a timely manner will ensure that year-end and quarterly financial statement audits and reviews will proceed as smoothly as possible and will also lead to greater shareholder and stakeholder transparency.

Kevin Cannon is a Director in Opportune LLP’s Valuation practice based in Houston.