© z_wei/iStock/Getty Images Plus

The COVID-19 pandemic has disrupted nearly every facet of our lives, both personally and professionally. Ironically, uncertainty is the only certainty in the wake of the virus. As the world scrambles to adjust to a new normal, accounting departments too are striving to quickly understand the impact the pandemic will have on financial reporting. One area of corporate financial reporting that could see a material impact from the virus is long-term asset impairment. During good times, accounting departments may overlook impairment asset testing, but in light of COVID-19, accounting teams should not ignore this important work as it is critical to ensuring the integrity of their company’s balance sheet(s).

No doubt, the negative economic impact of the virus justifies an impairment test for long-lived assets or asset groups for most industries. As an example, travel-related industries, such as airlines, are seeing widespread cancellations that could lead to cash flow challenges from their planes. Other examples of potential asset impairments that need to be tested include:

- Computers and systems that are built into offices or entire office buildings no longer in use due to remote working.

- Farming equipment that missed a season due to lack of demand.

- Idle assets such as movie theaters, restaurants and bars, and all related equipment.

The impairments are heavily dependent on factors such as the path of the virus, government restrictions on business operations, government aid, and consumer confidence.

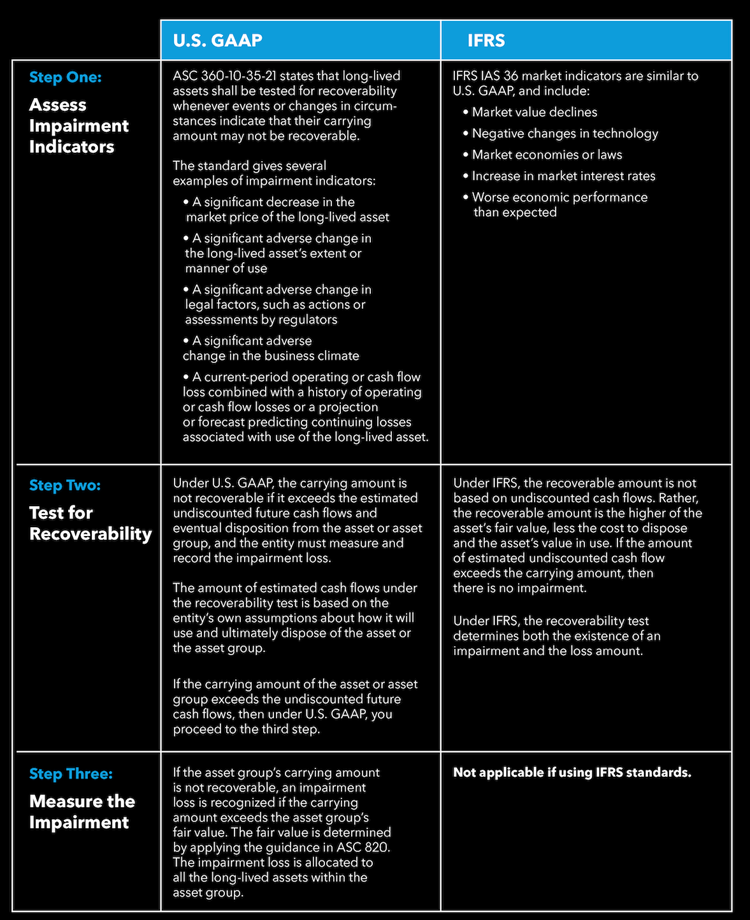

How to Determine if a Fixed Asset is Impaired

Depending on which standard is being used, impairment tests for long-lived assets should follow a two- or three-step process.

- Assess Impairment Indicators

- Test for Recoverability

- Measure the Impairment

Note, that in addition to the indicators below, an entity may identify other indicators that are particular to its business or industry. Once an indicator is identified, a company can test for recoverability.

Asset Impairment Loss Disclosures

Once an asset or group of assets are deemed impaired, key disclosures need to be made as noted below. In addition to utilizing standard guidance, entities should also look at what other companies are disclosing. Researching industry peers and market players to help guide impairment considerations and disclosures is advised.

US GAAP (ASC 360-1-50-2)

- Description of the impaired long-lived asset, including a description of the events and changes in circumstances that contributed to the impairment.

- The amount of the impairment loss and the caption in the statement of activities that includes the loss, if not separately presented on the face of the statement.

- The method or methods used to determine the fair value of the impaired long-lived asset.

Under IFRS (IAS 36, Paragraph 126 Disclosures)

- Amount of impairment loss

- Amount of any reversal

Planning for Future Recoveries

US GAAP does not allow for the reversal of a previously recognized impairment loss of a held-and-used long-lived asset. However, paragraphs 110 through 116 of IAS 36 allow an entity to reevaluate the recoverable amount of the asset to determine whether an impairment loss that was previously recognized still exists. Several examples of both external and internal information may indicate an impairment may no longer exist as noted below.

External Information Sources

- Observable indications that the asset’s value has increased significantly during the period.

- Significant changes with a favorable effect on the entity have taken place during the period, or will take place in the near future, in the technological, market, economic, or legal environment in which the entity operates or in the market to which the asset is dedicated.

- Market interest rates or other market rates of return on investments have decreased during the period, and those decreases are likely to affect the discount rate used in calculating the asset’s value in use and increase the asset’s recoverable amount materially.

Internal Information Sources

- Significant changes with a favorable effect on the entity have taken place during the period, or are expected to take place in the near future, in the extent to which, or manner in which, the asset is used or is expected to be used. These changes include costs incurred during the period to improve or enhance the asset’s performance or restructure the operation to which the asset belongs.

- Evidence is available from internal reporting that indicates that the economic performance of the asset is, or will be, better than expected.

Most companies are dealing with a wide range of challenges and changes in response to the COVID-19 market downturn. As the market continues to evolve, companies should continue to seek guidance from their technology partners and third-party experts to ensure they are handling capital assets, including asset impairment, in the best possible manner.

Joseph Bailey is Senior Accounting Analyst at Bloomberg Tax & Accounting. Shaina Lippman, CPA is a Business Analyst at Bloomberg Tax & Accounting.