.jpg?ext=.jpg)

© Jirapong Manustrong/iStock/Getty Images Plus

In August 2020, the FASB issued ASU 2020-06, Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity (“ASU 2020-06” or the “ASU”). ASU 2020-06 simplifies an issuer’s accounting for convertible instruments and its application of the derivatives scope exception for contracts in its own equity. Assuming a December 31 fiscal year-end, ASU 2020-06 is effective for public business entities, other than smaller reporting companies as defined by the SEC starting January 1, 2022. Adoption is delayed two years for all other entities. However, early adoption is allowed.

Entities not required to adopt the ASU on January 1, 2022, may consider early adoption for the following reasons:

- They currently have convertible debt subject to the cash conversion or beneficial conversion feature accounting models being eliminated under ASU 2020-06.

- They have equity-linked instruments classified as liabilities due to not meeting the requirements for equity classification (e.g., a freestanding warrant that required the company to post collateral or an embedded conversion option that did not meet the “own stock” scope exception because it allowed settlement in unregistered shares).

- They currently do not have the instruments noted above; however, they want to adopt the ASU to apply to new instruments prospectively.

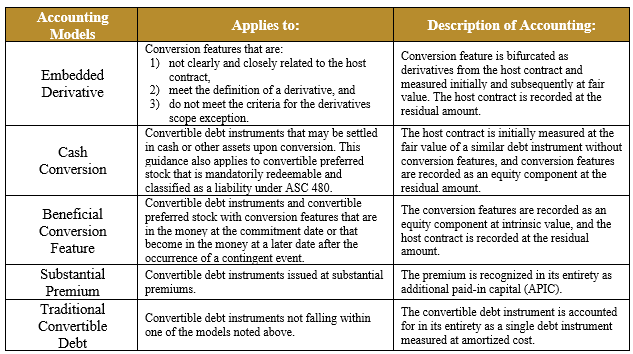

Convertible Instruments

Legacy GAAP Overview

Prior to the adoption of ASU 2020-06 (“Legacy GAAP”), there are five accounting models for convertible debt instruments. Except for the traditional convertible debt model that recognizes a convertible debt instrument as a single debt instrument, the other four models, with their different measurement guidance, require that a convertible debt instrument be separated (using different separation approaches) into a debt component and an equity or a derivative component. The following includes a summary of the accounting models listed in the order of how they should be applied.

The separation of a conversion feature generally creates a debt discount, which is subsequently amortized as interest expense over the term of the agreement, resulting in significant non-cash interest expense.

What Is Changing?

ASU 2020-06 removes the cash conversion and the beneficial conversion separation models. If the embedded conversion features are not required to be separated under the embedded derivative or substantial premium separation models, a convertible debt instrument will be accounted for as a single liability measured at its amortized cost, and a convertible preferred stock will be accounted for as a single equity instrument measured at its historical cost (assuming there are no other features requiring bifurcation and recognition as derivatives). By removing the cash conversion and the beneficial conversion separation models, the interest rate of convertible debt instruments typically will be closer to the coupon interest rate.

Why Is It Changing?

In receiving feedback from users of financial statements, the FASB found that:

- Most users do not find the current separation models for convertible instruments useful and relevant because they generally view and analyze those instruments on a whole-instrument basis.

- Many users also indicated that cash (coupon) interest expense is more relevant information for their analyses, rather than an imputed interest expense that results from the separation of conversion features required by GAAP.

ASU 2020-06 is intended to reduce the complexity of accounting for convertible instruments and to provide investors and other users of the financial statements with more meaningful information.

Contracts In An Entity’s Own Equity

Legacy GAAP Overview

ASC 815-40, Derivatives and Hedging—Contracts in Entity’s Own Equity, requires an analysis to be performed in the following situations:

- To apply a derivative scope exception for freestanding financial instruments and embedded features that have all the characteristics of a derivative instrument; and

- To assess whether freestanding financial instruments that potentially are settled in an entity’s own stock, regardless of whether the instrument has all the characteristics of a derivative instrument are required to be recognized as an asset or liability.

The analysis includes an assessment of the following two criteria:

- Is the contract indexed to an entity’s own stock?

- Does the contract meet the requirements for equity classification?

If the answer to either of these criteria is no, the contract is precluded from equity classification.

Under ASC 815-40-25, an entity must determine whether a contract meets specific conditions to be classified as equity (the “settlement criterion”). Analyzing whether a contract meets the settlement criterion involves evaluating the contract’s settlement optionality and conditions necessary for share settlement. The general concept behind the settlement criterion is that a contract that will settle in an entity’s own equity shares meets the criterion, whereas a contract that may (or will) require settlement in cash does not.

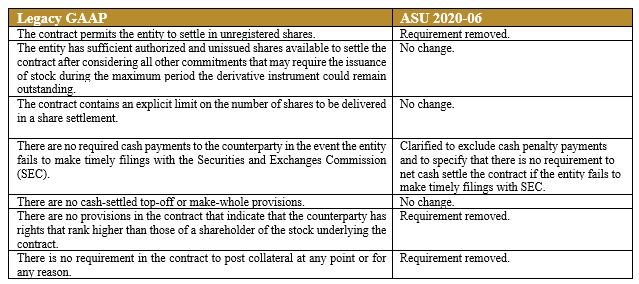

Because any contract provision that could require net-cash settlement precludes accounting for a contract as equity of the entity, legacy GAAP requires all the following seven conditions to be met for a contract to be classified as equity:

- The contract permits the entity to settle in unregistered shares.

- The entity has sufficient authorized and unissued shares available to settle the contract after considering all other commitments that may require the issuance of stock during the maximum period the derivative instrument could remain outstanding.

- The contract contains an explicit limit on the number of shares to be delivered in a share settlement.

- There are no required cash payments to the counterparty in the event the entity fails to make timely filings with the SEC.

- There is no cash-settled top-off or make-whole provisions.

- There are no provisions in the contract that indicate that the counterparty has rights that rank higher than those of a shareholder of the stock underlying the contract.

- There is no requirement in the contract to post collateral at any point or for any reason.

When performing this assessment, the guidance explicitly precludes considering the likelihood that an event would trigger cash settlement. Thus, a theoretical possibility of cash settlement being required would preclude the instrument from meeting the requirement to be classified in equity.

What Is Changing?

ASU 2020-06 removes three of the seven conditions noted above and clarifies another. These changes will change the population of contracts that are recognized as assets or liabilities and result in more contracts qualifying for equity classification. Below is a summary of the changes.

Why Is It Changing?

According to ASU 2020-06, the FASB received feedback that “the current guidance is rules-based, internally inconsistent, and often is asserted to result in form-over-substance-based accounting conclusions.” The Board decided to amend the guidance for the derivatives scope exception for contracts in an entity’s own equity to reduce form-over-substance-based accounting conclusions.

Transition Requirements & Considerations

For public business entities that meet the definition of an SEC filer, excluding entities eligible to be smaller reporting companies as defined by the SEC, the guidance is effective for fiscal years beginning after December 15, 2021, including interim periods within those fiscal years. For all other entities, the

guidance is effective for fiscal years beginning after December 15, 2023, including interim periods within those fiscal years. Early adoption is permitted, but no earlier than fiscal years beginning after December 15, 2020, including interim periods within those fiscal years.

Adoption can be applied on a modified retrospective basis or a full retrospective basis. Either method will require companies to calculate the impact of adopting the standard as if they had been applying ASU 2020-06 since the affected instruments were issued. This could require a significant amount of effort.

Additionally, while the changes from ASU 2020-06 are generally viewed as favorable, a company must fully assess all potential implications of early adoption. Examples of unfavorable results may include the potential reduction of interest eligible to capitalize (for companies that are currently capitalizing interest under ASC 835-20), increases in liability balances and the resulting potential unfavorable impact to debt covenants and financial ratios, and more strict rules regarding diluted earnings per share calculations.

Matt Smith is Managing Director at Opportune LLP.