©MARY GASCHO/ISTOCK/THINKSTOCK

The announcement Friday that Pfizer Inc. will buy back $11 billion of its own stock is the latest salvo in a nearly five-year frenzy of share repurchases by public companies. But many feel the buyback party is nearly over, and the resulting hangover will hinder corporate growth prospects for years to come.

“Buybacks are definitely at a relative peak,” says John Cryan, partner with corporate finance consulting firm Fortuna Advisors LLC. “More cash has been put into buybacks recently than anything that could drive earnings per share (EPS) growth, and that means less profitable growth in the future.”

Drug giant Pfizer is the latest big public corporate player to announce a massive buyback plan, announcing a $11 billion share repurchase that more than doubled the $5 billion share repurchase roadmap it announced in 2011. The drug company had $1.3 billion remaining on the original buyback prior to making the Friday announcement, which is reportedly in reaction to a failed deal to acquire AstraZeneca Plc..

But this is only the latest in a repurchase rampage that began nearly two years ago.

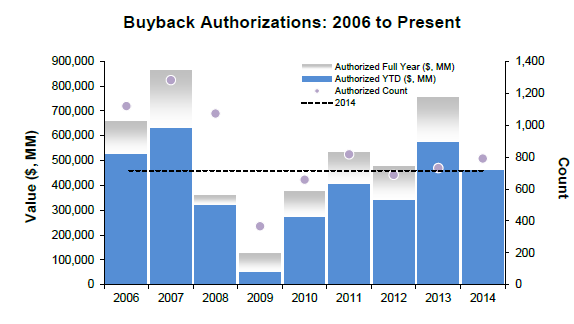

This year alone, there have been 791 share repurchase authorizations -- valued at $460 billion -- according to Westport, Conn.-based research firm Birinyi Associates. That is the fourth-largest buyback period of of all time, and 8 percent greater than the same period in 2013 (with 731 authorizations), according to the firm.

Chart courtesy of Birinyi Associates, Inc.

Share repurchases in the first nine months of this year were also the second-strongest period since the buyback bull market began in 2009, Birinyi Associates adds.

The resulting outcome of the half-decade buyback frenzy will likely be a significant slow-growth challenge for public company financial executives that went to the repurchase trough too many times, says Fortuna’s Cryan.

“The problem is that if you trace buybacks over time, many CFOs are repurchasing shares at the top of the market when they should be using that cash to invest back into the business and ignoring repurchases at historic lows,” Cryan says. “This really is the tail wagging the dog.”

Cryan explains that much of the share repurchases over the past several years were the result of “financial engineering” spurred by the U.S. Federal Reserve's quantitative easing program and the relaxed credit environment. The result are share repurchases that keep the value of shares artificially high while denying capital investment from “real” corporate growth drivers such as research and development, advertising or strategic acquisitions executed to enter new markets.

“More of cash flow is being put into buybacks at the top of the market rather than into new plants or research that will help corporate returns over the long term,” Cryan says. “That means overall lower growth for the future.”

For financial executives considering a buyback in the current market, Cryan says they need to answer two key questions:

- Are your shares trading at an intrinsic value discount, meaning are they undervalued independently of external factors like the credit environment?

- Do you have a credible plan to deliver on proving that intrinsic value to the market?

For those financial executives that ignore the hard questions around buybacks, the next several years will be tough.

“Many financial executives will realize that when they generated the most cash flow and had the most liquidity it wasn’t put into things that will set the company up for growth for the long term,” Cryan explains. “And when that growth isn’t there, you will not have the cash flow or liquidity to thrive. It just sets you up for a never ending cycle of slow growth.”