©peshkov/ISTOCK/THINKSTOCK

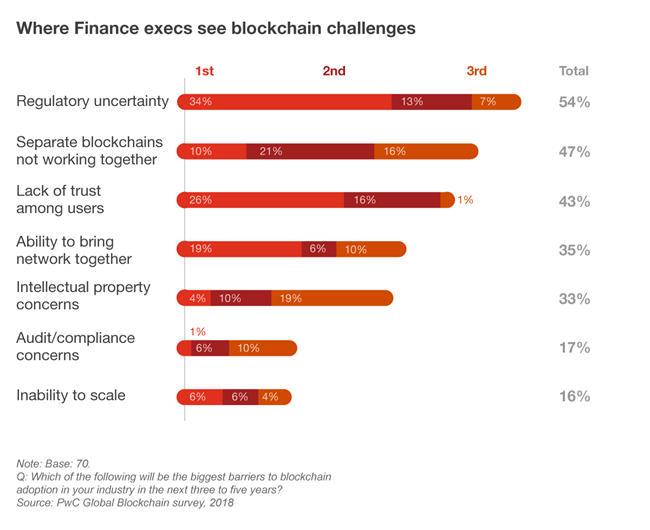

For the past several months, I’ve been espousing the many benefits of blockchain for finance. I truly believe this technology can significantly enhance the operations and effectiveness of finance organizations. Why, then, are some executives so hesitant to deploy blockchain? In a word: trust. And there are a number of dimensions to the issue, including questions around regulatory uncertainty, technology maturity, and user acceptance. For example, in PwC’s 2018 global blockchain survey, 26 percent of finance executives reported that a lack of trust among users was the number-one barrier to blockchain adoption. Another 17 percent ranked it as one of their top three concerns.

It’s human nature to be wary of new technologies, especially ones like blockchain that have the potential to revolutionize how business operates. But when the prospects are as favorable as those offered by blockchain, it’s counterproductive for finance executives to hold off.

An opportunity, not a threat

How can finance leaders convince the C-suite (and possibly themselves) that blockchain is worthy of consideration? To start, they should point out that trust is essentially the foundation of blockchain, which validates all transactions and delivers data accuracy and integrity. Finance executives must emphasize the fact that blockchain actually creates a trusted environment for enterprises and their stakeholders: customers, employees, suppliers, and vendors.

Then, to help move forward with your blockchain plans, we recommend these four strategies:

- Develop a strong business case for implementing blockchain — one that can result in measurable ROI. To do this, you will have to commit the finance organization to adopting new ways of working. You also will need to determine the challenges your department faces and the ways in which blockchain could help resolve them. Finally, you should start your blockchain initiative with a small pilot program and then scale up gradually.

- Consider the best ways for your finance organization to work with potential partners to build an ecosystem. Blockchain is more valuable when it’s part of a broader network, but getting stakeholders to agree on standards to define the business model is a tough challenge. It’s also important for finance executives to start with a small number of partners in the ecosystem and build it up over time. For example, a CFO could create an ecosystem that includes both internal partners, as well as external ones like vendors.

- Decide on an appropriate design. A finance ecosystem would necessarily be a permissioned blockchain, but you still need to determine levels of data access, among other things.

- Create a plan that enables your finance organization and other groups in your company to keep pace with the evolving regulatory environment. Regulations and laws about the protection of data can affect how your blockchain operates, so it’s essential to stay updated and be part of the engagement with regulators to help determine how this environment will change going forward.

By following these four strategies, you can build trust, along with a solid foundation for your blockchain, by convincing any reluctant parties — both in the finance department and in the company as a whole — that the numerous benefits of this technology far outweigh the challenges.

Michael Baccala is a PwC US Assurance Innovation Leader.