By Marc T. Macaulay

The audit profession and the organizations they serve recognize a data tsunami is on its way, with today’s consumers and businesses producing more data in a year than prior generations produced in their lifetime.

With the digitization of our society and our lives, everything creates data.

As a result, the auditing profession must develop and deploy advanced technologies to harness this explosion of data and unleash the insights embedded within it to advance audit quality and provide a deeper understanding of business and financial reporting risks, processes, and controls.

A recent Forbes Insights survey found 58 percent of auditors and businesses believe technology will have the single biggest impact on the audit over the next three to five years. And by 2020, smart machines will be a top-five investment priority for more than 30 percent of chief information officers. Perhaps that’s why more than two-thirds of CEOs in KPMG’s 2016 CEO Outlook survey said the next three years will be more critical for their industries than the previous 50 years.

What’s more, there’s widespread agreement that the impact of this innovation revolution will be positive for organizations that engage auditors: 59 percent of respondents to the Forbes survey agreed advanced technology will enable a deeper, more sophisticated analysis of data as part of the audit.

The power of cognitive technology, and how it will revolutionize the audit process, is breathtaking. The profound changes taking place in the audit space as cognitive technology evolves, combined with other innovative developments — such as robotic process automation (RPA) and advanced analytics — will change the auditing landscape permanently.

A New Imperative for Auditors

It’s imperative for audit firms to step up to this challenge to meet the ever-changing needs of the profession.

As businesses transform their operations to become more digital, and perhaps more global, many will be overhauling their IT systems with more sophisticated technologies. As a result, audit professionals must embrace the use of advanced tools such as data and analytics (D&A), RPA, automation and cognitive intelligence to manage processes, support planning and inform their decision-making.

What’s more, they’ll need to continue to develop innovative capabilities and technologies to maintain audit quality and strengthen the relevance of their audits into the future.

Audit Impact

Auditors once searched manually through reams of financial information to hunt down an anomaly that may have caused them to question the appropriateness of a client’s assertion. Now, thanks to innovative new technologies, the accumulation of almost unimaginable amounts of data and the application of advanced analytics and cognitive technologies make it possible to rapidly analyze far larger, more complete populations of financial and non-financial data.

These technologies can also generate richer, more detailed audit evidence for evaluation purposes, and provide business executives with:

• Actionable insights about their organizations, core processes and controls.

• Broader perspectives on the business and its risks.

What’s more, supervised cognitive systems can learn from each encounter with new information, enabling continuous refinement of the knowledge and analytical capabilities of the system.

As we will explore further in this article, auditors utilizing innovative technology will be able to deliver a higher-quality audit while providing deeper and more useful insights to their clients. For example, cognitive technology allows auditors to obtain and analyze information from non-traditional sources, including social media sites, TV, radio and the Internet, and determine if any of this external information may impact an audit either directly or indirectly.

In addition, the auditor can combine and process all of this information, together with the client’s own financial and other records and, through the use of advanced analytics, draw a deeper, more robust understanding of potential risks. These capabilities can also help increase the level of detail available for review and the speed with which very large amounts of data can be evaluated.

In combination with visualization tools, cognitive technology can bring audit information to life through automated charting and graphics that allow for a greater understanding of what’s been discovered, and promote timely and calibrated responses. For instance, these tools can provide clear illustrations of account relationships and transaction flows as well as anomalies in the data, both of which can offer a wealth of insights about a company’s controls, processes and performance.

The bottom line is that cognitive technology will enhance the ability of auditors to:

• Conduct a more detailed evaluation of financial and other information,

• Pinpoint data outliers and anomalies comprehensively, and

• Identify potential reporting, operations, or process issues more readily.

Cognitive Technology Basics

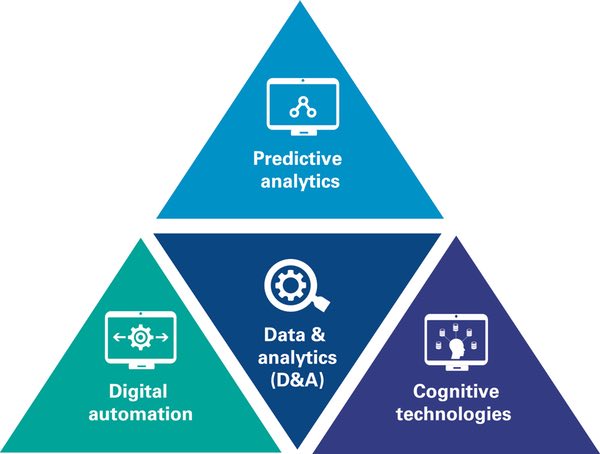

Cognitive technology (also frequently referred to as cognitive automation or artificial intelligence) essentially is an algorithm or chains of algorithms that enable software to absorb information, reason and think in ways similar to human beings. When combined with advances in digital and process automation, and data and analytics [see Figure 1], cognitive technology can have a profound impact across a broad spectrum of working environments and occupations.

The power and flexibility of cognitive technology is well-suited for professions where knowledge workers predominate. For example, the technology can be used to schedule airline flights and navigate airplanes from one location to another. Just as impressive is its impact in the medical profession, where highly sophisticated technology is used to diagnose disease and help doctors research effective treatment protocols.

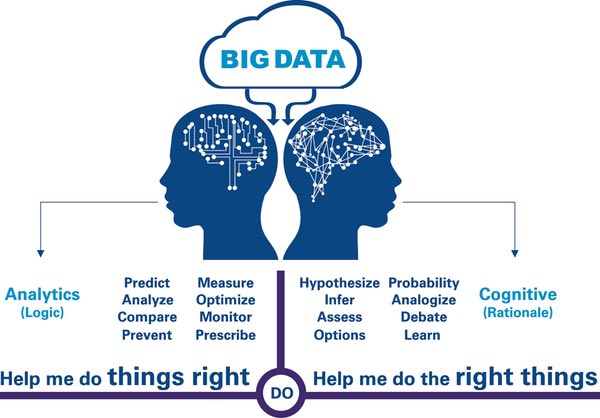

While cognitive and data and analytics are different [see Figure 2], they work together to generate greater analytic depth, broader perspectives and more effective decision-making. This combination of capabilities is essentially a force multiplier that can increase the level of detail and accuracy of audit processes, which in turn, enables auditors to sharpen their focus on higher-value audit activities and helps them deliver more insightful and effective audits.

How We Got Here

How We Got Here

The use of computer technology has been a mainstay in financial statement audits for decades. The programs traditionally used by auditors collected, organized and presented a limited sample of highly structured financial and select operational data.

However, cognitive systems deliver significantly more processing power and analytical capabilities. Cognitive intelligence mimics how the human brain works by analyzing data gathered from disparate sources and formats (including unstructured data1), generating hypotheses and making judgment-based decisions from the evaluation of supporting evidence.

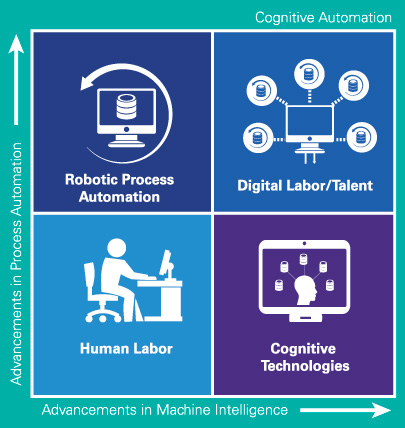

Cognitive automation represents the convergence of RPA and cognitive technology, which produces exponential increases in computer processing power and a foundation for artificial intelligence [See Figure 3].

Ten years ago, it couldn’t be done; the technology and the economics weren’t there. But the technology has arrived — machines can read documents, process language, learn, interpret, infer and evaluate data in powerful

new ways.

Equally important, though, is the vastly improved price point of technology. The advent of the cloud, combined with the decreasing cost and increasing power of computers, has resulted in a perfect confluence of factors driving the expanding use of this technology.

Cognitive Technology in Action

There’s no question cognitive technology will result in a seismic shift in the way audits are conducted. It integrates a combination of capabilities, including predictive analytics, pattern and image recognition, data mining and machine learning to evaluate information and deliver auditor-guided judgments across a variety of areas.

Below are some specific examples of how auditors will be able to apply cognitive technology to an audit.

Tackling revenue recognition: Consider the revenue recognition process of a large, global enterprise that offers multiple products and services and has hundreds, if not thousands, of contractual relationships. Errors in revenue recognition, even if inadvertent, can result in a tax, regulatory, and compliance nightmare.

Traditionally, an auditor would take a sample of transactions and, among other actions, examine the underlying source documents, evaluate the company’s accounting against the auditor’s judgments, and assess the reasonableness of its revenue recognition.

With the power of D&A and cognitive technology, however, while the process in theory is the same, a far greater percentage of transactions can be analyzed, and audit test work can be executed with greater global consistency. Advanced technology offers businesses operating in different parts of the world the ability to connect booked revenue with the appropriate contractual terms, and inform the auditor that a company’s method of booking revenue is either right, wrong or controversial.

The speed, depth and breadth of analysis simply cannot be matched by a human auditor alone, or even a team of auditors.

More “evidence-based” audit procedures relating to valuations: The valuation of assets or the determination of a company’s market value has long been a complicated and subjective area that is frequently subject to regulatory scrutiny. There typically are several possible methods on which to base a valuation, and there is often a measure of discretion and judgment involved.

As part of the audit of financial statements, the auditor may assess and test the reasonableness of a company’s valuation, including the underlying data, process and methodology used. In the past, auditors were limited by their ability, as human beings, to process the vast amount of available information.

Machine-augmented capabilities will dramatically change how valuations are audited. Auditors will be able to test the valuation controls more quickly and comprehensively than was possible in the past. Thus, they will, on a more timely basis, be able to make a judgment on the reasonableness of the organization’s valuation and explain why it is (or is not) reasonable.

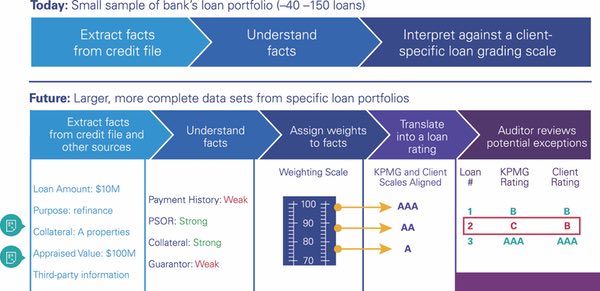

Bank loan portfolio analysis: Figure 4 offers an illustration of how cognitive technology can be used in an audit of a bank’s loan portfolio. It will allow auditors to gain a more detailed and comprehensive understanding of credit risk and potential audit exceptions based on loan grading.

The use of cognitive technology will produce a better understanding of a company’s risks and overall control environment that can enable auditors to focus their attention on areas of heightened risk or control weakness.

The examples on the prior pages are just the beginning of what can be accomplished with cognitive technology. Given the enormous processing power of cognitive technology, it’s almost impossible to know all of the benefits it will offer to clients and the audit profession in the future.

Ultimately, it could provide auditors with opportunities to continuously monitor the design and effectiveness of internal controls, and identify emerging or expanding risks.

The Human Element: Still Critical

Sometimes lost in the talk about the potential benefits of cognitive technology is the fact that an audit professional still needs to be at the helm of the engagement. Cognitive technology undoubtedly presents a powerful, and eventually, indispensable tool in the audit process.

But at the end of the day, it’s the auditor who makes the critical decisions and offers the key analysis and insights in the audit of an organization’s financial statements.

To use a chess analogy, many people may recall how in 1997, IBM’s “Deep Blue” chess program beat then-world champion Gary Kasparov in a six-game match. But far fewer know that more recently, when a person familiar with chess was teamed with a computer, the team consistently prevailed over another super computer — or expert chess player, for that matter — acting alone.

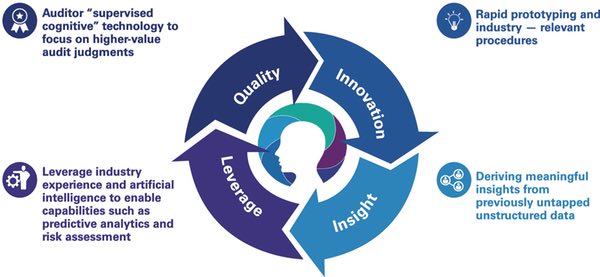

That’s why “supervised cognitive” technology — the combination of cognitive capabilities with the skills and knowledge of audit professionals — will be the best approach to conducting an audit [see Figure 5]. The ability of cognitive technology to conduct analyses, draw insights and employ “learned judgment” will be a tremendous supplement to the auditor’s decision-making responsibility. Because in the end, the auditor is the one who must make the final call on the audit opinion.

Final Thoughts

Final Thoughts

We are creating data faster than ever and, given this explosion of data, audit firms must combine innovative technologies with the skills and knowledge of qualified professionals to remain relevant.

In this environment, teams of professionals must possess more than just an understanding of accounting and auditing — they need stronger critical thinking, analytical, data science and IT skills to complement their financial and business acumen. The profession will need to continue to work with universities, regulators and leading technology companies to enhance the skill sets of its people and develop new capabilities to advance audit quality.

At the same time, audit firms making significant investments in these powerful advanced technologies demonstrate their commitment to delivering high quality audits that dig deeper into the data and reveal more about a business and its risks. Equally important, it helps them deliver audits with deeper insights on an organization’s controls, accounting practices and reporting processes.

1. Unstructured data refers to information that doesn’t reside in a traditional row-column database. Rather, it is information that is contained in other formats or sources such as e-mails, free text documents, videos, photos, audio files, presentations, and Web pages.

Marc T. Macaulay is KPMG’s US Cognitive Technology Audit Leader, where he is responsible for the development and implementation of a cognitive technology strategy in support of the firm’s US Audit practice. He can be reached at [email protected].

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation. The KPMG name and logo are registered trademarks or trademarks of KPMG International. © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.